Let’s Talk Mortgages

The purchase of a home is one more step along life’s winding road. Regardless of the size or type of home, it’s an opportunity to put a roof over your head that you can actually call your own. But to many, a home purchase requires borrowing a large amount of money, and therefore acquiring a large debt that most have never experienced. It is this debt that the following will help to explain.

Documents Required For Financing

When applying for a mortgage, it is important to have all the necessary documents prepared in advance. When a lender has many applications to process, it is easy to understand that those that are the most complete will get attention first. To ensure your application is looked at promptly, try to obtain as many of the following as possible.

Income Confirmation

Though T4’s and pay stubs are often suitable to begin financing, a salary letter from all employers will be required. It should confirm annual income, position, length of time on the job and be on company letter head. For self-employed individuals, the last two years’ Income Tax Return, Notice of Assessments and/or financial statements are often required.

Down Payment Confirmation

Whether it is money in your bank account (usually a 90 day history of the account is required), RRSP’s, term deposits, or a gift from family, your down payment must be confirmed. Take along a copy of all certificates, statements or bank books. If the money is a gift from a family member, a “gift letter” specifying that it is a non-repayable gift will be needed, as well as confirmation of the gift being deposited into your account. Eliminate any concerns a lender may have regarding the source of your down payment. Proper documentation now will prevent questions later.

Accepted Offer to Purchase

This is a written contract that shows the price, terms and conditions under which a buyer agrees to purchase a property from a vendor. It will be signed by both the purchaser and vendor and witnessed by a third party. If it is a private purchase, the lender will require both vendor and purchaser to have separate lawyers. If it is a purchase listed through the MLS system, an offer to purchase written up by a licensed real estate agent is acceptable. If you have not yet purchased a home, an offer is not required to get your mortgage pre-approved.

Feature Sheet or Listing on Property

This provides a lender with a brief description of the property to be mortgaged. If you have not yet purchased a home, have an idea of purchase price, property taxes, and condo fees if applicable, on the type of home you would be interested in.

Assets & Liabilities

Put together a list of assets and existing debts that you may currently have. Regardless of how much or how little, a lender needs this information to determine how much mortgage you would qualify for. The more accurate this information, the quicker and more complete the application process will be.

Definitions

AMORTIZATION – The actual number of years it will take to repay the mortgage in full. The longer the amortization, the smaller the monthly mortgage payment. A commonly used amortization period is 25 years or less.

CANADA MORTGAGE AND HOUSING CORPORATION (CMHC) or GENWORTH or CANADA GUARTANTY – These organizations provide insurance to financial institutions who lend up to 95% of a property’s value. The insurance premium is paid by the borrower and can cost up to 3.15% of the actual mortgage amount. This premium is added to the mortgage being borrowed.

CLOSING DATE – The date on which the purchaser takes legal possession of the property. At this time the lawyers will transfer funds from the purchaser to the vendor and title of the home to the buyer. Also known as the Possession Date.

CONVENTIONAL – MORTGAGE A loan that is secured by a mortgage registered against the property. It never exceeds 80% of the appraised value of the property or the purchase price, whichever is less.

HIGH RATIO MORTGAGE – A conventional mortgage that exceeds 80% of the property’s value. This mortgage must be insured by CMHC or Genworth.

SURVEY – A document that shows accurate measurements of land and improvements on a property. If a survey is not available, the lenders will insist on title insurance being arranged on your behalf.

TERM – In a mortgage, “term” is the actual length of time for which the money is loaned at a set rate of interest. Terms are commonly from 6 months to 5 years, though longer terms may also be available. After the term expires, you can either repay the balance owing or re-negotiate the mortgage at current rates and conditions with the lender.

VENDOR – The individual(s) selling a property.

COLLATERAL MORTGAGE –A mortgage that has as its primary security a promissory note or loan agreement and as “backup,” a collateral security, being a mortgage registered against your property. A collateral mortgage cannot be assigned, therefore at this time a collateral mortgage cannot be transferred to another lender on maturity without cost. Therefore, on maturity, eliminating your ability to shop around for a better rate. If possible, avoid collateral mortgages.

Do I Qualify?

Most institutions offer a pre-approved mortgage that tells you in advance the amount of mortgage you are approved to borrow. This calculation is based on your income, down payment, and any debts you currently have. It can also hold a current mortgage rate for up to 120 days while you look for a home.

The normal banking system allows home buyers to use up to 39% of their gross monthly income towards housing costs (GDS), which includes mortgage payment, property tax and heating. If the property purchased is a condominium, ½ of monthly condo fees must also be added. As well, up to 44% (T.D.S.) of gross monthly income can be spent on these housing costs and any other debts (i.e.: car loans and credit card debt).

If your credit bureau has a Beacon Score of under 680, lower ratios may apply.

As of the fall of 2017, the government came out with new “Stress Test” borrowing guidelines, that impact all borrowers. The new “rules” state that if you have LESS than 20% down payment, we must use a rate of 5.34% in qualifying you, regardless of the rate that I get you for the mortgage.

If you have MORE than 20% down payment, I must use the contract rate of your mortgage PLUS 2%. Therefore, if your rate is 3.79%, I have to use 5.79% in qualifying you.

In summary, remember that more important than qualifying within the guidelines of an institution, is your sense of comfort with the monthly payments. Do a detailed family budget to ensure what you want to pay, and with that we can confirm if it is inline with what the system allows.

Example: Pre-Approved Mortgage

Qualifying Process – First Step

Assume you are purchasing a condominium for $300,000.00. Your mortgage is $240,000.00 at 3.75%, with a 25 year amortization. Your gross annual income is $65,000.00 (or $5,416 per month). Because we are using 20% down payment, and the rate is 3.75, I have to use a rate of 5.75% in qualifying (3.75 +2= 5.75%) In the example below I have used a mortgage payment based on 5.75% (even though the rate you will get will be 3.75%).

Qualifying Process – Last Step

The final step in qualifying is to look at what other debts you have. For example, any loan or credit card payments must be added to the above housing costs and the total cannot exceed 44% of your gross monthly income. Assume your monthly car payment is $300.00.

See chart below.

Is Rate Really Everything?

Rate is always foremost in people’s minds when inquiring about a mortgage. It does warrant concern, because a difference in rate directly affects your monthly mortgage payment. But rate is not everything! Two institutions may have the same rate for a specific term, and yet the privileges offered may be quite different. Ensure that any mortgage you take has good prepayment, is portable and increasable, and offers bridge financing. Make sure it also isn’t registered as collateral, unless it is necessary for your purposes (i.e. getting a secured L/C). Don’t compromise accepting a mortgage with limited privileges to get a slightly better rate, it could be a costly mistake.

Portable

A mortgage should be portable, meaning you can take the existing mortgage with you to a new property being purchased. The new home must be acceptable to your institution.

Assumable

An institution should allow the purchaser of your home to assume the existing mortgage. He must qualify though, as you did. The reason behind having an assumable and portable mortgage is that when selling your home, the mortgage won’t have to be discharged. If you discharge an existing mortgage during the term, the penalty can be substantial.

Increasable

A mortgage should always be increasable, meaning that during the term of your mortgage you can increase the amount of the loan for a specific purpose. An example would be borrowing money to build an addition consolidate debt etc.

Prepayment Privileges

Most mortgages, unless specified otherwise, are closed. A closed term means that the mortgage cannot be paid off prior to maturity. So to make long term mortgages attractive, most institutions allow some form of prepayment option. A common example of this would be a 15+15% option. You can pay up to 15% of the original mortgage loan once each year and or you can increase your monthly payment by 15% once a year without penalty. These privileges can vary from one lender to the next.

Payment Frequency

All institutions should give the borrower an option of paying their mortgage monthly, weekly, or bi-weekly. How your salary is paid may dictate to you which is more convenient, however paying your mortgage on an accelerated weekly or bi-weekly (i.e. accelerated bi-weekly is your monthly payment divided by 2, and paid every 2 weeks) basis will pay your mortgage down faster than if paid monthly. Ask how this can benefit you.

Unexpected Costs You May Have

Mortgage Setup Costs

When arranging a mortgage there are legal and disbursement costs (i.e. courier, registration fees etc.) associated with that process. A lawyer is required on all home purchases to transfer clear title of the property from the seller to the buyer. Legal fees, which I will assume include their disbursement costs and taxes (do not confuse with land transfer tax) are the responsibility of the purchaser.

For the bank to approve a mortgage, they are normally required to have an appraisal and or insurer approval. If CMHC/Genworth/Canada Guaranty are involved there is tax (do not confuse with land transfer tax) that the government charges on the insurance premium. These costs could add up to 1% of the mortgage amount. When your offer to purchase is accepted, ask what costs are applicable to you.

Tax Hold Back

Many lenders require that property taxes be collected with your monthly mortgage payment. They then send these payments directly to your municipality.

The lender usually requires sufficient funds in your “tax account” to pay any incoming property tax bills. To ensure this, the lender could hold back a portion of your estimated annual property taxes from the mortgage advance. This money is not lost, but put aside in your “tax account” so that sufficient funds are always available to pay your property taxes.

What it means to you though is that your down payment required will increase by the amount of the hold back. Every lender can deal with property taxes differently, so as you can see, it is an important question to ask!

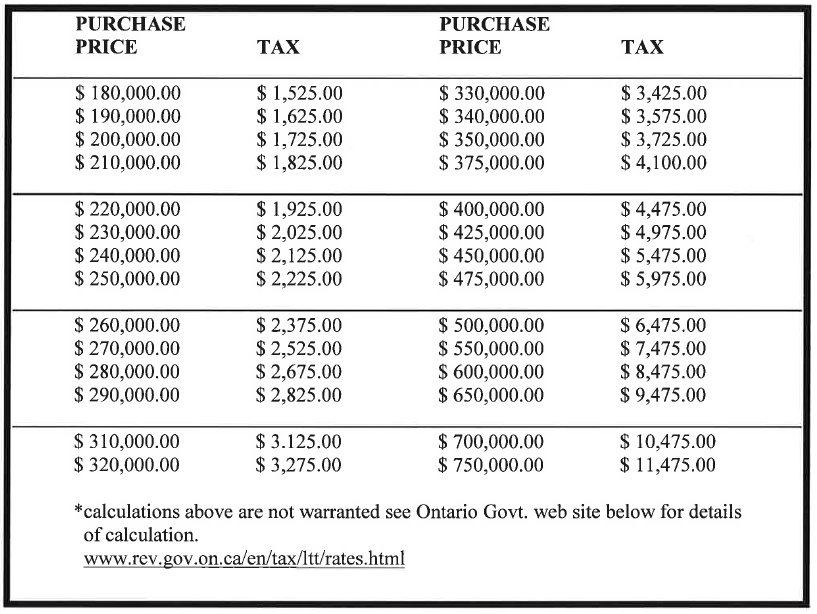

Land Transfer Tax

Unlike property taxes, land transfer tax is a one time cost paid by the purchaser on closing. It is similar to the tax you pay on a store bought item, but due to the size of a home purchase, it can be a significant expense. Use the chart (below) to determine the estimated tax based on your particular purchase price. First time borrowers today, receive an immediate $2,000 reduction on their property land transfer tax. Check with your lawyer to see if this applies to you.

Where to borrow

Where to obtain a mortgage is a common concern among home buyers. The likely place to inquire would be where an individual does their personal banking, but is this source of funds always the best source of funds? The answer is often no.

All institutions have different rates, prepayment options and terms. It’s up to you, the borrower, to ensure that the mortgage suits your needs. You should not have to conform to the needs of the bank. Does the institution have flexible hours of business, and after hour access to a knowledgeable individual? Is the institution offering competitive rates and privileges? Does the loans officer you will meet, have the authority to approve your mortgage?

To simplify the search for your mortgage, why not use the experience of a mortgage broker? A mortgage broker has access to funds from all institutional lenders, from banks to life and trust companies that the general public may not be aware of.

By having access to such a broad range of lenders, the home buyer is guaranteed the best possible rates and privileges. A lender is found that suits your needs, not the banks.

Most mortgage brokers are accessible evenings and weekends, to answer questions and approve loans during office hours that are convenient to you. For most qualified home-buyers, there are no broker fees for arranging a mortgage. The fees of a mortgage broker are paid by the institution that funds your mortgage, usually a percentage of the mortgage amount. So with guaranteed lowest rates, flexible hours of business, and no broker fees, the service of a reputable mortgage broker can take the financial worries out of purchasing a home.

Ottawa-Carleton Mortgage Inc. is a registered Mortgage Brokerage #10419 with the Financial Services Commission of Ontario.

MORTGAGE PAYMENT CALCULATOR

For an online application click the “Apply Now” button. You will be providing us with personal information about yourself and your mortgage needs over a SECURE SERVER. I will contact you within 24 hours to follow up and provide the best mortgage rates available for your needs.

If you would prefer to do an application “offline”, simply click on the “Application Download” button, complete the application, sign it, and fax or scan it back to me.

If you would prefer to make an appointment, I would be more than happy to sit down with you to discuss your needs. I can take your information in person, and answer any questions you may have.

My direct cell# is 613-720-5348

I believe the more you know and understand about mortgages, the less worry you will have.

Chris Faubert